How to divorce when you own a business together

When a business-owning couple decides to divorce, understanding how business valuations and state marital property laws intersect becomes crucial. The valuation process directly affects how assets are split, influenced by varying state statutes. This article explains these complex interactions and guides you through what to expect in divorce-related business valuations and state marital property laws.

Please read the top strategies for a business divorce valuation.

Key Takeaways

- Accurate business valuation is essential in high-net-worth divorces for equitable asset division, tax implications, and future financial planning.

- State marital property laws and the classification of businesses as marital or separate property significantly influence divorce asset distributions.

- Engaging qualified business valuation experts and forensic accountants is crucial for preventing disputes and ensuring fair valuations during divorce proceedings.

- Small business owners need to know the fair market value of their business and what percentage of the company they own is marital assets.

- The valuation date is important in a divorce business valuation. Is it the separation date or the filing date used in the business valuation date?

The Role of Business Valuation in Divorce

In the realm of high-net-worth divorces, business valuation plays a pivotal role. Accurate business valuation ensures an equitable division of assets. This process assigns a specific value to the business, significantly influencing the separation of assets and liabilities. Business valuation experts provide the precise assessments needed for fair distribution.

State laws further complicate the process as they determine the applicable standards of value, which can vary significantly from one jurisdiction to another. Knowing these standards shapes the outcomes of asset division in divorce proceedings.

Beyond merely dividing assets, a thorough business valuation helps shape strategic post-marital decisions concerning finances, alimony, and future investment strategies. Business valuation is not just about numbers; it secures a fair and sustainable financial future for both parties in a divorce.

Importance of Accurate Valuation

Accurate valuation is crucial for fair asset division in divorces. In divorce business valuations, two standards of value are commonly accepted. These are fair market value and fair value. Fair market value is the price at which an asset would change hands between a willing buyer and a willing seller, while fair value is an accounting standard used to measure assets and liabilities. Correct standards are essential, as incorrect ones can lead to expert opinions being dismissed by the court.

The valuation process involves assessing various aspects of the business, including intellectual property, customer relationships, business debts, and business liabilities, to derive an accurate worth. Business valuation experts ensure a thorough and precise process, facilitating an accurate valuation.

An accurate valuation impacts the immediate division of assets and future financial planning. Understanding the business’s present value and potential future earnings allows both parties to make informed decisions regarding alimony, investment value, and other financial matters.

Valuing professional practices are often asset-light businesses that rely heavily on past and future cash flows to determine the present value of the business interest.

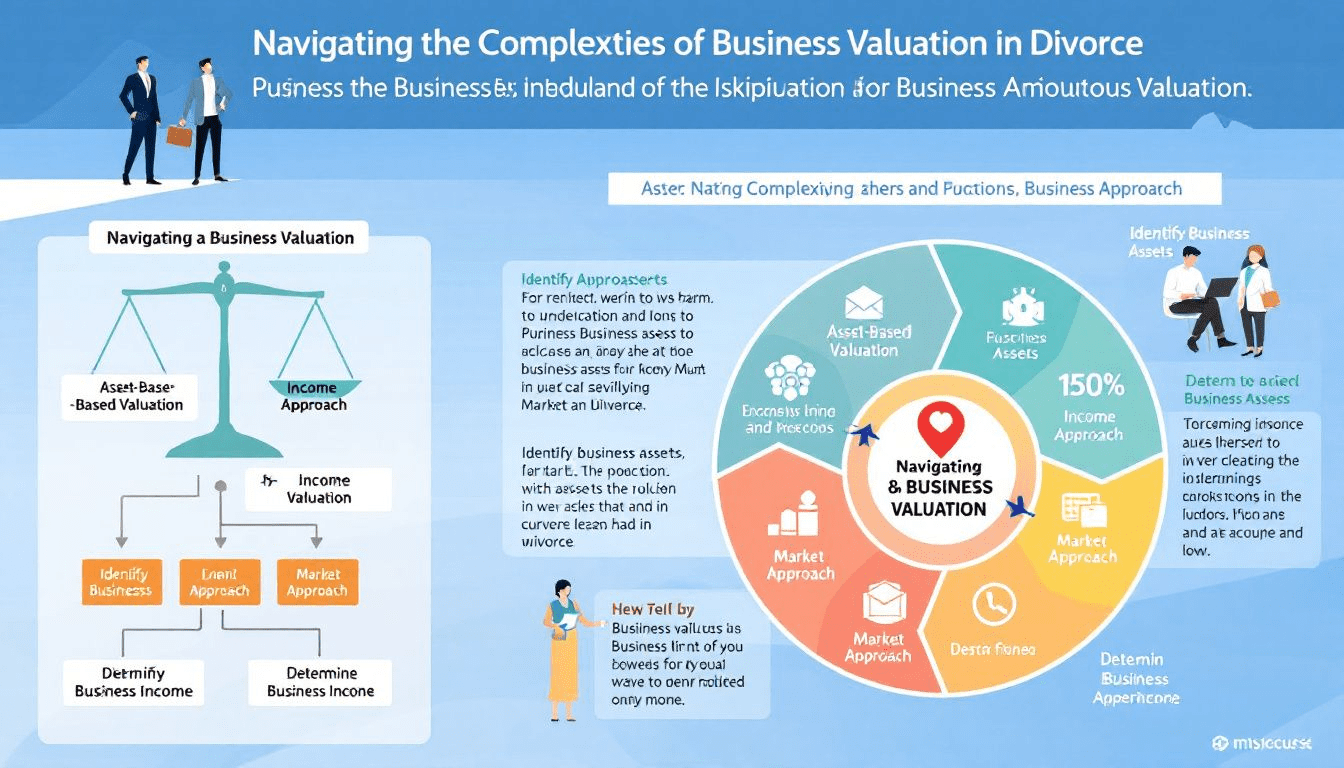

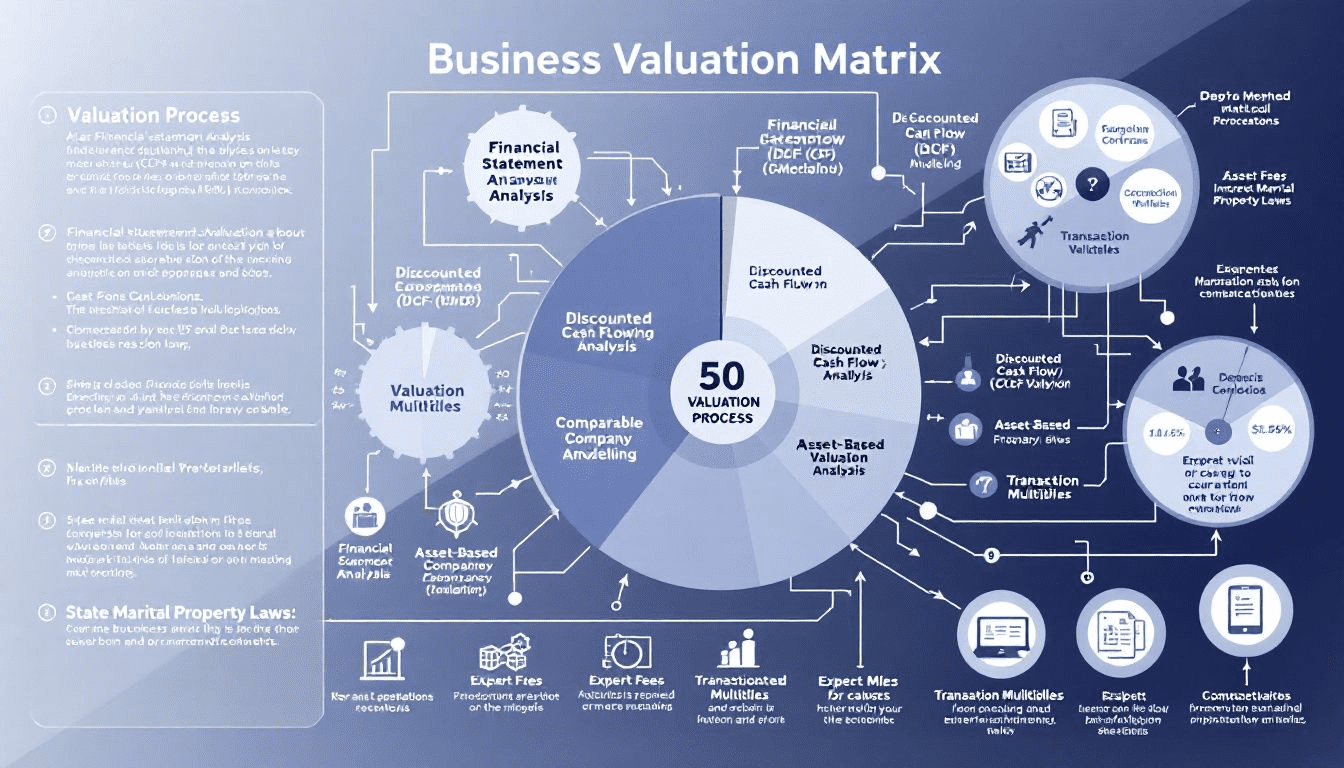

Common Valuation Methods

Business valuations employ various methods to determine the value of a business. The three main approaches are the asset approach, the market approach, and the income approach. Each method offers a unique perspective on the business’s value, so choosing the correct method based on the specific circumstances is key.

The asset approach calculates a company’s value by subtracting liabilities from total assets. This method is beneficial for businesses with significant tangible assets.

On the other hand, the market approach uses the sale prices of similar businesses to estimate a company’s value. This method is beneficial for businesses in competitive and well-documented industries.

The income approach assesses a business based on its expected future earnings. This method considers projected future revenues and expenses, providing a dynamic view of the business’s potential.

Business valuation experts are crucial in applying these methods accurately to ensure a fair and reasonable valuation.

Understanding Marital Property Laws

Marital property laws significantly influence the division of assets during divorce proceedings. Marital property includes assets acquired during the marriage, while separate property includes assets owned before marriage and gifts and inheritances given explicitly to one spouse. Determining whether a business is a marital or separate property adds a layer of complexity to the valuation process.

State laws play a crucial role in this determination, as they dictate how business interests are classified and valued. For instance, in Pennsylvania, a business is classified as a marital asset, subjecting it to equitable distribution during divorce proceedings. Knowing these laws is crucial for high-net-worth divorces, as they directly impact asset division outcomes.

The classification of business interests as marital or separate property can significantly affect the division of assets. Thus, understanding state-specific marital property laws and their application to business interests is vital.

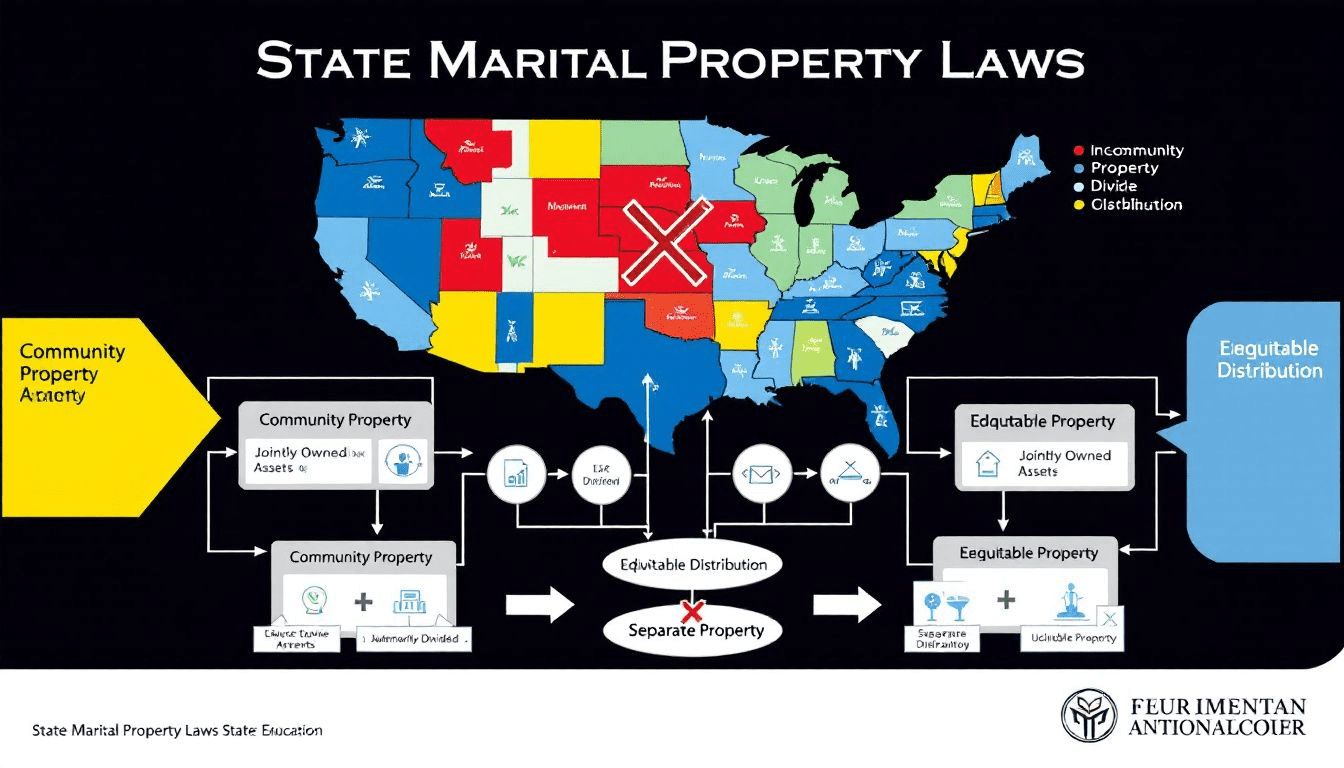

Community Property vs. Equitable Distribution States

Community property and equitable distribution states handle the division of marital property differently. Community property states consider all assets acquired during the marriage as jointly owned and divide them equally upon divorce. This strict 50/50 split approach simplifies the division process but may not always be fair.

Equitable distribution is a system by which certain states divide property during a divorce. Marital property assets are divided based on a fair distribution, which does not necessarily mean equal. These states consider various factors, such as spouses’ contributions and needs, leading to potentially unequal distributions.

Grasping these divorce distribution differences is crucial for navigating high-net-worth divorces.

Defining Marital and Separate Property

Defining marital and separate property is a critical step in the divorce process. Marital property includes assets gained during the marriage, while individual property encompasses assets owned before marriage, gifts, and inheritances given explicitly to one spouse. This distinction is vital as it determines which assets are subject to division.

Business valuation plays a crucial role in clarifying ownership stakes and determining if a business qualifies as a marital asset. Agreements such as prenuptial or postnuptial agreements can specify that any increase in business value after marriage will be treated as marital property. These agreements provide clarity and help prevent disputes during asset division.

Grasping the distinction between marital and separate property ensures fair and equitable asset division. It ensures that each party receives their rightful share and helps avoid contentious legal battles.

Impact of State Laws on Business Valuations

State laws significantly impact how business valuations are conducted during divorce proceedings. These laws influence the division of business assets, affecting the financial outcomes for both parties. Understanding a business’s actual fair market value can facilitate mediation and lead to more amicable divorce settlements.

Accurate business valuations prevent disputes regarding asset distribution. This is especially important for businesses in sectors such as healthcare and technology, where valuations can be particularly complex. Attorneys and valuation experts must consider the jurisdiction’s statutes and case law when valuing businesses in divorce cases.

Past cases provide valuable guidance on the characteristics of value standards and allowable procedures in business valuation. These precedents help ensure valuations are conducted fairly and consistently, leading to equitable asset division.

Community Property States

In community property states, businesses acquired during the marriage are typically considered joint assets. Any business value acquired during the marriage is considered joint property and divided equally upon divorce. This approach simplifies the division process but may not always reflect the contributions of each spouse.

Community property states divide assets equally, while equitable distribution states allow courts to distribute marital property based on fairness, which may not equate to a 50/50 split. Understanding these differences is crucial for anyone involved in high-net-worth divorces.

Equitable Distribution States

Equitable distribution states, such as Pennsylvania, handle asset division differently. They consider various factors, distinguishing them from the equal division common in community property states. This fairness-based approach allows for a more nuanced division of assets, considering each spouse’s contributions and needs.

Because equitable distribution states may lead to unequal distributions, individuals need to understand how these factors can impact their asset division during divorce. This understanding helps ensure that the division of assets is fair and equitable.

Challenges in Business Valuation During Divorce

Valuing a closely held business within divorce is fraught with challenges. Unique business factors must be carefully analyzed, including company-specific risks and historical financial performance. Aligning income reporting with actual business performance is often complicated for closely held businesses.

Goodwill, an intangible asset, presents additional valuation challenges due to its subjective nature. Business owners may also hide income, reallocate assets, or inflate expenses, leading to inaccurate valuations related to personal goodwill. These issues must be addressed to ensure a fair and accurate valuation.

Double Dipping

Double dipping is a significant challenge in business valuations during divorce. This term refers to the unfair scenario where the same income is counted twice—once in the business valuation and again in alimony calculations. This can place an undue financial burden on the spouse responsible for paying alimony.

One common way double dipping occurs is when the owner’s salary for business valuation differs from that used for calculating alimony. Addressing double dipping ensures a fair division of assets and support obligations.

Hidden Income and Inflated Expenses

Another challenge in business valuation during divorce is the potential for hidden income and inflated expenses. Business owners may conceal or transfer assets, understate revenue, or overstate expenses to protect their financial interests during divorce. This manipulation can significantly distort the perceived profitability and valuation of the business.

Forensic accountants uncover hidden assets and ensure accurate financial reporting. They meticulously analyze financial records to identify discrepancies and provide expert valuations crucial for equitable property division.

The involvement of forensic accountants helps uncover the true financial state of a business, ensuring that both tangible and intangible assets are accurately assessed. This, in turn, provides a fair division of marital assets.

Using Experts in Business Valuation

Engaging business valuation experts ensures accurate and fair outcomes. Forensic accountants and business valuation experts provide the precision and reliability needed in these complex evaluations. Their expertise ensures thorough examination and accurate reporting of all aspects of business value.

Consulting a divorce attorney can help identify reputable business evaluators experienced in divorce-related valuations. Choosing a qualified evaluator is critical, as their experience and methodology can significantly impact the valuation process.

Valuation experts bring technical skills and credibility to the valuation process, especially in cases involving financial fraud or income dishonesty. Their insights can significantly influence judicial decision-making in divorce cases.

Role of Forensic Accountants

Forensic accountants are invaluable in the business valuation process during divorce. They help determine a business’s value, assist in separating marital from non-marital assets, and may provide testimony in court. Their involvement becomes crucial if there’s suspicion of financial fraud or manipulation by one of the spouses.

Forensic accountants provide critical insights into financial records and identify fraudulent business valuation activities. Their expertise ensures that all pertinent financial information is accurately represented in divorce proceedings.

Selecting a Qualified Business Evaluator

Choosing a qualified business evaluator ensures fair and accurate valuations. Choosing an evaluator with relevant experience and credentials specific to business valuation in divorce cases is important. This ensures precision and dependability throughout the evaluation process.

Evaluators with courtroom experience are particularly valuable, as their insights can significantly influence judicial decisions. Engaging a qualified divorce valuation expert helps facilitate efficient valuations and ensures the valuation process is objective and fair.

Costs Associated with Business Valuation

Typical Divorce Valuation Cost Range

The costs associated with business valuation can vary significantly based on the complexity and purpose of the valuation. For most business owners, the cost typically ranges from $3,700 to $9,700. For small businesses, valuation costs usually range from $2,700 to $5,700, while larger companies may incur costs from $10,000 to $50,000.

In high net-worth divorce cases, business valuation expenses can exceed $50,000, especially for complex valuations. Knowing these costs helps in planning and budgeting for the valuation process in high-net-worth divorces.

This underscores the importance of planning and budgeting for business valuation costs in divorce proceedings.

Specialized Valuation Costs

Specialized business valuations, such as those for IRS or court purposes, range from $4,900 to $11,000 plus court time if needed. Valuations for SBA loan purposes typically cost between $2,700 and $5,700. These costs reflect the specific requirements and complexities associated with each type of valuation.

Other specialized valuations include selling to a family member, which ranges from $4,900 to $10,900, and selling to employees, which ranges from $4,900 to $11,000. Knowing these costs is essential for accurate financial planning and aligning the valuation process with its intended purpose.

Protecting Your Business Assets

Protecting business assets during divorce ensures that owners retain control over their enterprises. Implementing prenuptial and postnuptial agreements can explicitly state that a business is a separate property, thereby limiting its division in a divorce. These agreements maintain owner control and prevent the company from being classified as part of the marital estate.

Succession plans and buy-sell agreements are also crucial in protecting business assets. These agreements outline how ownership of a business will transition, protecting its value and ensuring stability. Establishing clear ownership and operational guidelines can help prevent disputes regarding business assets during a divorce.

Prenuptial and Postnuptial Agreements

Prenuptial and postnuptial agreements serve as formal legal documents that specify the ownership and division of business assets in case of separation or divorce. These agreements can prevent a business from being classified as part of the marital estate, thus maintaining control for the owner. Legal counsel for both spouses enhances their enforceability in court when drafting these agreements.

Clearly defining ownership distinctions between marital and separate property in these agreements minimizes disputes and protects personal business interests. They provide a safeguard for business owners, ensuring that their enterprises remain intact and operational despite marital issues.

Succession Plans and Buy-Sell Agreements

Succession plans and buy-sell agreements protect business assets during divorce proceedings. These formal agreements can clarify ownership distinctions and provide guidelines for asset division, ownership assignment, and transfer restrictions. This ensures that a business can continue operating without disruption in the event of a divorce.

By incorporating buy-sell agreements, business owners can determine who will buy out the other partner’s share, providing stability and continuity for the business. These agreements, alongside effective business valuation, enhance asset protection and reduce conflicts in marital property division.

Summary

Understanding business valuations and state marital property laws is crucial for navigating high-net-worth divorces. Accurate business valuations ensure a fair division of assets and liabilities, significantly influencing the financial outcomes for both parties. Engaging business valuation experts and forensic accountants provide the precision and reliability needed for these complex evaluations.

State laws, whether community property or equitable distribution, play a pivotal role in determining how business assets are divided. Clear distinctions between marital and separate property and prenuptial and postnuptial agreements help protect business interests and ensure fair asset division.

Business owners can confidently safeguard their assets and navigate the complexities of high-net-worth divorces by understanding the challenges and employing strategies such as succession plans and buy-sell agreements. Remember, thorough preparation and expert guidance are key to securing a fair and sustainable financial future.

Frequently Asked Questions

How can accurate business valuation impact divorce settlements?

Accurate business valuation is crucial in divorce settlements as it determines the specific value of the business, which directly affects the fair division of assets and liabilities. This ensures an equitable outcome for both parties involved.

What is the importance of business valuation in divorce beyond asset division?

Business valuation is crucial in divorce as it informs strategic post-marital financial decisions, including alimony determinations and future investment strategies. This ensures a fair and equitable financial arrangement for both parties involved.

What can lead to inaccurate business valuations during divorce?

Inaccurate business valuations during divorce can occur due to business owners concealing income, reallocating assets, or inflating expenses. These actions compromise the integrity of the valuation process, leading to unfair outcomes.

What is the typical cost range for most business valuations?

The typical cost range for most business valuations is between $2,900 and $9,700. This range can vary based on the complexity of the business and the type of valuation required.

What is the cost of a business valuation for IRS or court purposes?

The cost of a business valuation for IRS or court purposes typically ranges from $4,900 to $11,000, with additional expenses for court time if applicable.