Depreciation and Capital Expenditures

Depreciation allocates the cost of assets over time, impacting financial statements. Without cash outflow, it still represents a crucial business expense. This article explores why depreciation is a real expense and its financial implications.

Key Takeaways

- Depreciation is an essential accounting practice that allocates the cost of fixed assets over their useful life, aiding in accurate financial representation and long-term planning.

- As a non-cash expense, depreciation does not directly impact a company’s cash flow but significantly influences net income and tax liabilities, thus affecting overall financial health.

- Different depreciation methods can alter financial statements, influencing investor perceptions and business valuation; understanding these methods is critical for effective financial management.

- Assets depreciate over time. The company must budget Capex every year to replace worn-out or obsolete equipment.

- The market value of the assets will vary significantly from their depreciated value.

Understanding Depreciation

Depreciation is a fundamental accounting practice reflecting the reduced value of fixed assets over time. Contrary to the common belief that depreciation merely signals asset loss, it serves a more intricate role. Depreciation spreads the cost of an asset over its useful life, matching expenses with the revenues it generates and adhering to the matching principle in accounting.

Imagine purchasing a piece of equipment for your business. Instead of recognizing the entire cost in the year of purchase, depreciation allows you to allocate this cost over several years, reflecting the asset’s gradual wear and tear. This provides a more accurate financial picture and stabilizes your income statement by avoiding large, one-time expense deductions.

Depreciation is not just about balancing books; it is essential in long-term financial planning. For instance, building depreciation is factored into investment decisions and asset management strategies, ensuring that the real estate value and cash flow are accurately represented. Understanding how depreciation works can significantly influence financial decisions and business sustainability.

Please read how inflation can destroy business value.

Depreciation as a Non-Cash Expense

Depreciation is classified as a non-cash expense, meaning it does not involve actual cash outflows. This distinction is crucial because it affects how financial statements record and present depreciation. While depreciation reduces net income on the income statement, it does not directly affect the company’s cash balance. This separation helps avoid a substantial expense deduction in the asset purchase year, smoothing out earnings over time.

In accrual accounting, depreciation is recognized even if no cash transaction occurs, reflecting the gradual loss in the value of a tangible asset. This practice ensures that financial statements provide a realistic view of the company’s financial health. For instance, a company’s cash flow statement will add back depreciation to net income in the operating activities section, clarifying the cash generated from operations.

It’s a common misconception that depreciation affects cash flow. In reality, depreciation does not lead to an immediate cash outflow. By understanding this, businesses can better manage their financial strategies, recognizing that while depreciation reduces taxable income, it doesn’t impact the company’s cash reserves directly.

Impact on Financial Statements

Depreciation impacts various financial statements, shaping the perception of a company’s financial performance. Depreciation expense reduces the net income reported on the income statement, reflecting the cost of using fixed assets over time. This reduction can affect investor perceptions and the overall company profitability assessment.

On the balance sheet, depreciation lowers the value of fixed assets, impacting the company’s overall financial position. Accumulated depreciation is recorded in a contra account, offsetting the asset’s original cost. This practice ensures that the balance sheet accurately represents the net book value of the company’s assets.

Income Statement Effects

Depreciation is recorded annually on the income statement as a non-cash cost, reflecting the wear and tear of fixed assets over time. This indirect operating cost reduces gross profit and, subsequently, operating income and net income. Reduced net income from depreciation can lead to lower reported earnings, potentially affecting financial analysts’ assessments of the company’s performance.

The reduction in operating income and the company’s net income due to depreciation is significant. For instance, if a company records a high depreciation expense, it might report a lower net income, potentially resulting in a loss. This impacts the company’s profitability and tax obligations, as depreciation expenses reduce taxable income.

Depreciation’s impact on the company’s income statement highlights the importance of understanding how this non-cash expense influences overall financial health. It reflects a gradual decrease in asset value, ensuring that the financial statements provide a realistic picture of the company’s operational costs and profitability.

Balance Sheet Implications

On the balance sheet, accumulated depreciation reduces the carrying value of fixed assets, indicating a decrease in the overall asset value. This reduction is recorded in a contra account, which serves to offset the fixed asset’s initial cost, ensuring that the net book value accurately reflects the asset’s current worth.

The net book value of an asset is calculated by subtracting the accumulated depreciation from the asset’s original acquisition cost. This calculation provides a realistic assessment of the asset’s book value, which is crucial for financial reporting and asset management. But NOT its fair market value or replacement cost. Accurate depreciation practices enable businesses to evaluate their financial position better and make informed investment decisions.

By understanding the balance sheet implications of depreciation, companies can ensure that their financial statements accurately represent the actual value of their assets and balance sheets. This realistic financial positioning is vital for maintaining investor confidence and planning future capital expenditures (CapEx).

Depreciation Methods

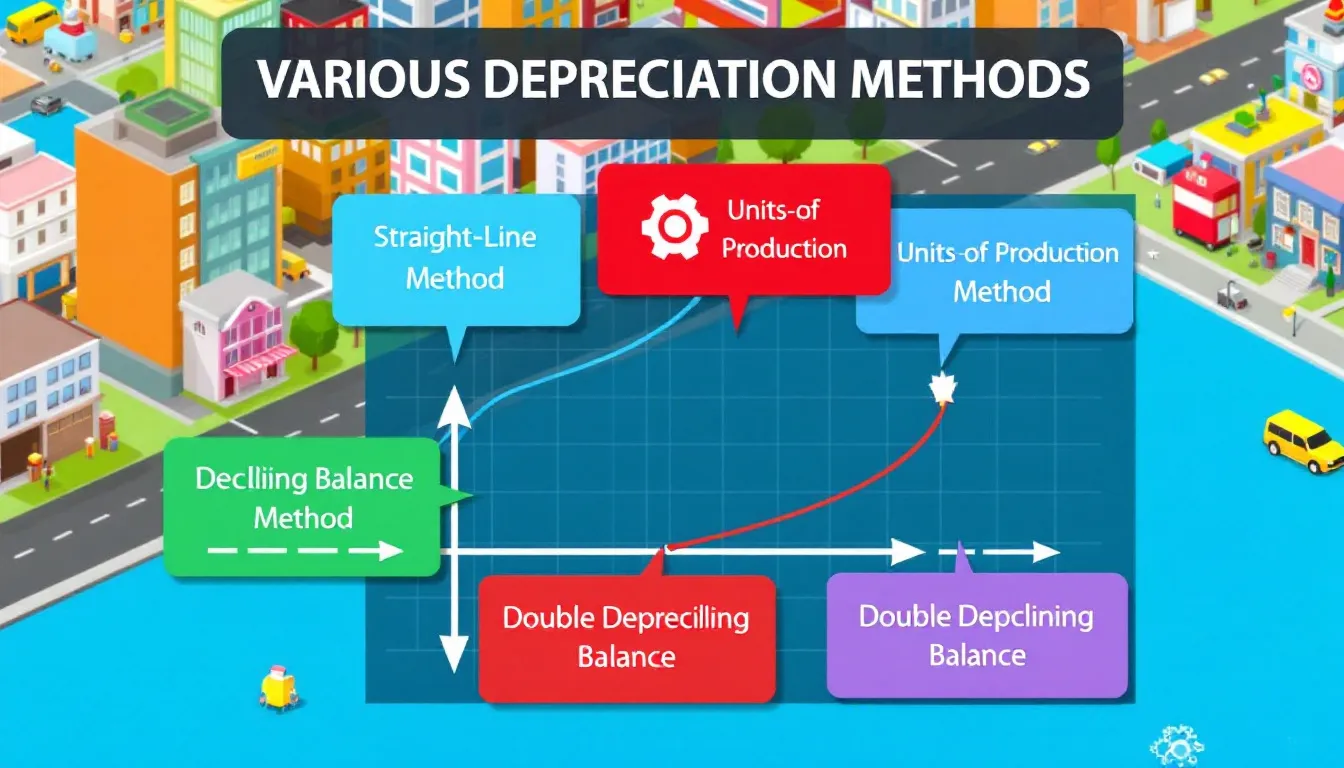

Different depreciation methods can significantly affect a company’s financial statements, influencing reported earnings and tax liabilities. Generally accepted accounting principles (GAAP) permit four methods:

- Straight-line

- Declining balance

- Sum-of-the-years’ digits

- Units-of-production

Each method has its unique approach to allocating the cost of an asset over its useful life.

The simplest method to calculate depreciation expense is the straight-line depreciation method, which divides the asset’s cost evenly over its estimated useful life. This approach provides a consistent annual depreciation expense, making it easy to record and understand. For example, if a machine costs $200,000 and has a useful life of 10 years, the annual depreciation expense would be $20,000.

The declining balance method, on the other hand, results in higher depreciation expenses during the initial years, decreasing over time. This method accelerates the depreciation process, reflecting the higher usage and wear of assets in their early years. Similarly, the sum-of-the-years’-digits method combines features of both straight-line and declining balance methods, yielding higher depreciation in the earlier years.

Units-of-production depreciation links the expense to the actual usage or output of the asset. This method benefits manufacturing equipment, where the depreciation expense correlates with the number of units produced.

The correct depreciation method is essential for accurate financial reporting, affecting the company’s balance sheet, income statement, and overall financial strategy.

Tax Benefits of Depreciation

Depreciation offers significant tax benefits by allowing businesses to deduct depreciation expenses from their taxable income, leading to potential tax savings. This deduction reduces the income subject to taxes, effectively lowering the company’s tax liabilities. For instance, a company that purchases machinery for $500,000 can claim a depreciation expense of $50,000 yearly over ten years, significantly reducing its taxable income.

The recognition of depreciation affects taxable income, providing a valuable tax relief opportunity for businesses. Depreciation deductions help companies manage their tax obligations more effectively by reducing taxable income, freeing up resources for reinvestment and growth. This mainly benefits businesses with substantial capital expenditures, as they can leverage depreciation to optimize their financial performance.

The Internal Revenue Service (IRS) mandates depreciation for certain assets, allowing deductions over time and offering tax relief. By understanding and applying the appropriate depreciation methods, businesses can strategically manage their income taxes and enhance their overall financial health.

Real-World Examples of Depreciation

Practical examples of depreciation help illustrate its application in real-world scenarios. For instance, when machinery is sold, the calculated loss due to depreciation can significantly impact financial statements. This reported loss also influences tax liabilities by reducing taxable income, highlighting the importance of understanding machinery and equipment depreciation for accurate financial representation.

Building depreciation is another critical area, reflecting the loss of value of a building over time due to factors such as wear and tear, age, and market conditions. Recording building depreciation as an expense over its useful life allows companies to spread the acquisition cost over multiple periods, impacting net income, cash flow management, and future capital expenditure budgeting.

Machinery and Equipment

Regarding machinery and equipment, understanding depreciation is crucial for accurately representing a company’s financial position. For example, if machinery is sold at a loss due to depreciation, this loss can significantly impact financial statements, reducing taxable income and affecting tax liabilities. This highlights the importance of recording depreciation accurately to ensure realistic financial reporting.

Moreover, the depreciation of machinery and equipment plays a vital role in tax planning, as it reduces taxable income and optimizes the business’s financial performance. Companies can better manage their financial health and make informed investment decisions by accurately calculating and recording machinery depreciation.

Building Depreciation

Building depreciation reflects the loss of value of a building over time, influenced by factors such as wear and tear, age, and market conditions. This depreciation is recorded as an expense over the building’s useful life, allowing companies to spread the acquisition cost over multiple periods and ensuring that the financial statements accurately represent the asset’s value.

Effective management of building depreciation is crucial for long-term financial planning, as it influences net income, cash flow management, and budgeting for future capital expenditures. Applying the appropriate depreciation methods ensures accurate financial reporting and helps maintain investor confidence.

Depreciation in Cash Flow Statements

Depreciation is classified as a non-cash expense, meaning it does not involve actual cash outflows. The cash flow statement adds depreciation expense to net income in the operating activities section, providing a clearer picture of the cash generated from operations. This adjustment is crucial for evaluating a company’s actual cash-generating performance.

Considering depreciation in cash flow evaluations allows financial analysts to better gauge the company’s operational efficiency and financial health. This practice ensures that the cash flow statement accurately reflects the company’s cash inflows and outflows, providing valuable insights for decision-making and financial planning regarding cash flows.

Depreciation vs. Amortization

The primary difference between depreciation and amortization lies in the types of assets they apply to. Depreciation is for tangible assets, such as machinery and buildings, while amortization is for intangible assets, such as patents and goodwill. Both processes help match expenses to revenues, providing a more accurate financial representation.

Common methods used for both depreciation and amortization include the straight-line method, where the cost of the asset is evenly distributed across its useful life. Understanding these methods and their application is crucial for accurate financial reporting and strategic financial management.

The Role of Depreciation in Business Valuation

Depreciation significantly affects business valuation by lowering reported earnings, which can influence perceived profitability. Utilizing depreciation allows companies to strategically manage their tax obligations and enhance cash flow, impacting overall financial health.

The reduction of asset value through depreciation directly impacts return on equity metrics, as equity is derived from assets minus liabilities. This can lead to lower investor assessments and affect the company’s valuation.

The right depreciation method is essential for accurate financial reporting and business valuation. Different methods can alter financial statements, influencing investor perceptions and strategic financial decisions.

Assets must be adjusted from depreciated book value to fair market value when valuing a company.

Please read understanding add-backs when selling a business.

Common Misconceptions About Depreciation

One prevalent misunderstanding is that depreciation is an immediate expense upon asset purchase. However, depreciation is capitalized and distributed over the asset’s lifespan, ensuring expenses are aligned with the revenue they help generate. This practice adheres to the matching principle in accounting, which requires that expenses be recorded in the same period as the expected generated revenue.

Another misconception is that all forms of depreciation are the same. Different depreciation methods can lead to varying impacts on reported income and tax liabilities. Understanding these nuances is crucial for accurate financial reporting and strategic financial management.

Many times, for tax purposes, assets are 100% expensed in the year they are purchased. This is why book value is a poor predictor of an asset’s current and remaining value.

Summary

Depreciation is a vital accounting practice that reflects the gradual loss of value of fixed assets over time. It is crucial in balancing expenses, reducing taxable income, and providing a realistic financial picture. Businesses can strategically manage their financial health and tax obligations by understanding various depreciation methods.

In conclusion, depreciation is more than just an accounting term; it’s a powerful tool for long-term financial planning and business valuation. Businesses can ensure accurate financial reporting and maintain investor confidence by demystifying depreciation and recognizing its true impact on financial statements.

Frequently Asked Questions

How does depreciation affect net income?

Depreciation decreases net income by being recorded as an expense on the income statement, which reflects the allocation of fixed asset costs over their useful lives. This reduction highlights the financial impact of asset usage on overall profitability.

What is the difference between depreciation and amortization?

Depreciation is applied to tangible assets like trucks, machinery, and buildings, whereas amortization relates to intangible assets like patents, formulas, and copyrights. Both processes serve to align expenses with revenues over time. But both can distort assets’ fair market value or replacement cost.

How do different depreciation methods impact financial statements?

The choice of depreciation method significantly affects reported income and tax liabilities, which in turn influences a company’s overall financial picture. As a result, businesses must carefully consider their depreciation strategy to ensure accurate financial representation.

What are the tax benefits of depreciation?

Depreciation provides tax benefits by lowering taxable income, which results in potential tax savings and enhanced cash flow management. This can significantly aid in overall financial planning.

Please read how to read a tax return.

Why is understanding depreciation important for business valuation?

Understanding depreciation is crucial for business valuation as it impacts reported earnings and return on equity, thereby shaping investor perceptions. Accurate valuation hinges on recognizing how depreciation reflects the true financial health of a business.

In most instances, an asset’s depreciated value is far different from its fair market value or replacement cost.